Irs Section 42 Lihtc Program

Https Www Irs Gov Pub Irs Utl Irc42 Low Income Housing Credit Atg Part 7 Pdf

Form 1040 What Is Still Deductible Deduction Child Tax Credit Investing Money

Irs Provides Temporary Relief For Lihtc Nahb Now The News Blog Of The National Association Of Home Builders

Http Nlihc Org Sites Default Files Ag 2018 Ch05 S09 Lihtc 2018 Pdf

Letter Of Intent Lease Template Elegant 39 Letter Of Intent Templates Free Word Documents In 2020 Free Word Document Marketing Plan Template Printable Letter Templates

Http Berkshireseniorcommunities Com Wp Content Uploads 2015 07 Berkshire Section 42 Pdf

Tenant qualifications for section 42 tax credit programs.

Irs section 42 lihtc program.

Guide To Irs Form 5695 How To Claim The Federal Solar Tax Credit Tax Credits Federal Taxes Tax Time

Https Www Novoco Com Sites Default Files Atoms Files Letter Tenantdata Final 032610 Pdf

Why Project Is A Defined Term In Lihtc Irc Section 42 Youtube

Irc Section 42 Low Income Housing Tax Credits And Irc Section 47 Hist

Irs Provides Section 42 Covid 19 Relief National Center For Housing Management

Https Www Nhlp Org Wp Content Uploads Ohio Lihtc Lawsuit Pdf

Developers And Cities Are Navigating The Affordable Housing Sea In A Leaky Boat Next City Low Income Housing Affordable Housing Development

Https Www Novoco Com Sites Default Files Atoms Files Virginislands Programsummary 07 Pdf

3 21 3 Individual Income Tax Returns Internal Revenue Service

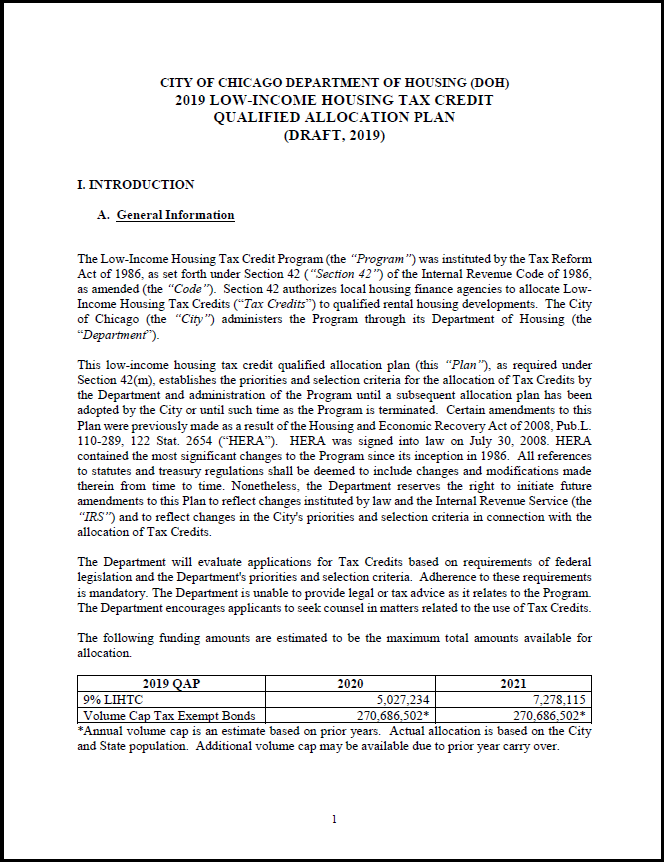

City Of Chicago Qualified Allocation Plan

Instructions For Form 1040 Nr 2019 Internal Revenue Service

How To Use The Irs Withholding Calculator With Images Child Tax Credit Budgeting Tips Budgeting

3 11 3 Individual Income Tax Returns Internal Revenue Service

Pin On Silhouette Projects

Http Www Mhdc Com Program Compliance Documents Faq Pdf

How The Self Employed Can Minimize Their Taxes Quickbooks Filing Taxes Irs Taxes Tax Extension

Affordable Housing Guide Apartmentguide Com

Calendar Real Estate Infographic Real Estate Information Housing Market

If You Are An Individual Who Did Not Pay Your Last Installment Of Estimated Tax You May Choos Accounting Help Child Tax Credit Estimated Tax Payments

Understanding Taxes Essay Outline Student Elgin High School

Can Technology Pick The Perfect Health Plan For You Obamacare Health Care Health Insurance

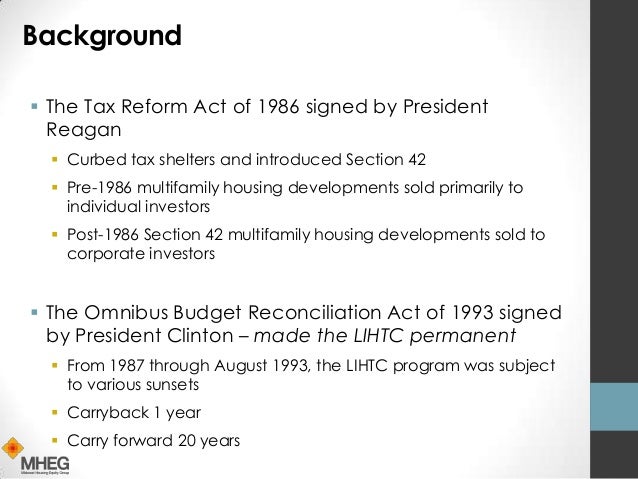

Lihtc Low Income Housing Tax Credit Program Compliance Ppt Download

Https Dhcd Dc Gov Sites Default Files Dc Sites Dc Page Content Attachments Lihtc 20owners 20cert 20of 20continuing 20program 20compliance 202017 Pdf

Https Www Treasurer Ca Gov Ctcac Programreg Proposed Regulation Changes Pdf

Source : pinterest.com